Is FORO (Fear Of Running Out) ruining your retirement?

Every week we deal with countless examples of people fearful of running out of money in retirement due to uncertainties about future expenses and longevity. Rising healthcare costs, inflation, and market volatility can erode savings faster than expected and add to the negative rhetoric.

Having spent a lifetime accumulating wealth for retirement, it is not uncommon to see people unable to switch from an accumulation mindset to decumulation. This financial insecurity can lead to anxiety, and it often holds back retirees from spending money and pursuing things they always dreamed of.

The perfect antidote is to remove as much uncertainty as possible from the equation and focus on the controllables. Whilst we can’t remove uncertainty entirely, having a better understanding of what to expect in retirement can better prepare you for what is to come. You can learn from those who have come before you.

Having successfully supported clients for over 30 years, our business has gained considerable insight into financial decision making and lifestyle choices in retirement. We have navigated clients through significant financial, economic, and social changes including the Global Financial Crisis, 9/11 and more recently the COVID-19 outbreak. We have also helped clients celebrate personal and family milestones, navigate life’s ups and downs and unfortunately, we have seen many of the heartaches and tragedies that life can sometimes throw your way.

Sharing with you some key observations we have noted over the years supporting retirees may help give you some confidence about your retirement outlook.

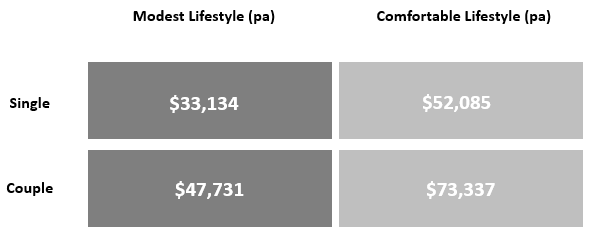

- Knowing how much you are likely to need to spend in retirement can assist with adequately planning for retirement and creating a savings goal. As a benchmark, the Australian Superannuation Fund Association (ASFA) regularly release a retirement standard. This will help you understand if your retirement income aspirations are reasonable, bearing in mind it is okay not to be “average”.

- Another easy way to determine your retirement income needs is to ask yourself, is my/our current income from work sufficient for my day-to-day needs. Would you be comfortable replacing your work income in retirement? If so, use it as your retirement cash flow goal.

- The adage ‘leopards don’t change their spots’ typically rings true. We rarely see people who have lived a financially conservative life overspend in retirement hence your pre-retirement income is a good starting point.

- People learn to live with what they have. If you happen to “spend up” early in retirement and your wealth has dwindled, it often happens over the course of many years giving you time to adjust to a potentially lower income later in life.

- Supporting this notion, you will typically spend more per year from 60-75 than you do from 75-95. There are times when we encourage clients to enjoy their wealth. To take the holiday they have dreamed about, and then take another! Over time you can lose your passion for travel, pampering and adventure, or worse still, your ability to do so.

- If you own your home, it is possible to access equity via the Government Home Equity Access Scheme or a reverse mortgage. This is a great safety net and can help you access funds from what might be your biggest asset.

- We live in the “lucky country” and with a bevvy of Government support available, you will never go without.

- Money simply gives you choices. The more money you have, the broader your financial and lifestyle options tend to be. Relying solely on Government support will limit your choices, though you can still get by.

Our key takeout – You should take comfort from the sacrifices you have made to secure your retirement. It is now time to enjoy it!

Having put such a positive tone to the above observations we are certainly not suggesting you become financially irresponsible, but we do recommend you enjoy what you have worked so hard to accumulate.

Our final and perhaps most important observation is that seeking advice from qualified professionals is invaluable when considering your retirement needs. With legislation around Superannuation, Pensions, Tax and Retirement already complex enough and constantly changing it can be extremely beneficial both financially and from a ‘peace of mind’ perspective to engage a financial professional to support you in retirement.